This comprehensive article explores the intricacies of ACH (Automated Clearing House) transfers, a pivotal facet of electronic funds transactions. Covering types, history, and operational mechanisms of ACH transfers, the piece provides a thorough comparison with alternative payment methods.

What is an ACH transfer?

An ACH transfer falls under the category of electronic funds transfers, with two distinct types: ACH debit and ACH credit. ACH debit is employed for various transactions such as paychecks, expense reimbursements, government benefits, tax refunds, annuity payments, and interest disbursements. On the other hand, ACH credit is utilized for point-to-point direct payments.

Whether initiated by an individual, a company, or an organization, ACH transfers facilitate direct payments between bank accounts. Popular online payment applications like Venmo and Zelle leverage this method for seamless money transfers between parties, essentially involving the movement of funds from one bank account to another.

In 2020, the United States witnessed over two billion ACH transfers, marking a notable 15.2% increase from the previous year. While some of this surge may be attributed to pandemic-induced social distancing measures, it is evident that ACH transfers are gaining widespread popularity as a preferred mode of payment.

History of the Automated Clearing House

The automated clearing house, established in 1974, is overseen by the National Automated Clearinghouse Association (NACHA)), acting as a self-regulating body responsible for the ACH network's management and administration, including the formulation of its rulebook.

ACH emerged in response to the surge in paper checks during the 1970s, causing strain on the banking system. This U.S.-based electronic system interconnects banks, credit unions, and various financial institutions.

Presently, the ACH network boasts more than 10,000 connected financial institutions, processing a staggering 25 billion electronic transactions annually, with a cumulative dollar volume exceeding $55 trillion. Its applications extend to various electronic funds transfers, encompassing credit cards, direct deposit, and pay-by-phone systems.

ACH transfers: How they work

The initiation of an ACH transfer occurs when the sender, using their bank or a payment processing service, triggers the process. Payroll companies and bill-paying software, such as BILL, also facilitate ACH transfers, ensuring timely payments for employees on direct deposit or individuals seeking expense reimbursement.

Recent technological advancements have led to substantial improvements, particularly in reducing payment times. While some ACH transfers already offer "instant" availability, achieving network-wide capabilities across all institutions is still in the developmental phase.

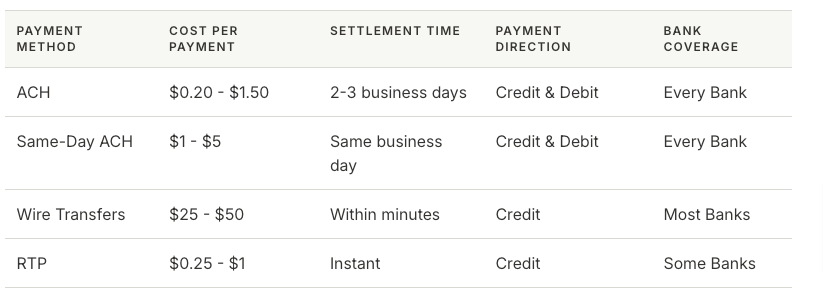

How does ACH compare to other payment methods?

When comparing payment methods, it's essential to assess their speed, cost, coverage, and supported directions. Speed is commonly measured by settlement time, indicating how long it takes for funds to transfer from the originating to the receiving account. Cost is evaluated per payment, while coverage considers the number of banks and financial institutions in the US supporting the payment method. The supported direction is also crucial, as methods like ACH facilitate both pulling (debiting) from and pushing (crediting) funds to a counterparty's bank account, whereas others like Wires only support pushing.

To provide a comprehensive overview, let's compare ACH and same-day ACH with Wire Transfer and RTP, two other prominent electronic payment methods in the United States.

ACH Payments - Advantages and Benefits

FISPAN facilitates ACH payments for its users, harnessing the many advantages associated with this form of electronic funds transfer. Leveraging the Automated Clearing House (ACH) settlement system offers several benefits:

- Convenience: Utilizes secure networks to expedite fund transfers across a variety of transactions without imposing daily maximums.

- Affordability: Generally entails lower costs compared to alternative digital fund transfer methods.

- Speed: While some payments are processed almost immediately, certain transfers may take up to four days to complete.

- Tracking: Establishes a comprehensive record of all transaction activities.

- Security: Implements encryption for enhanced security and typically employs contactless payment protocols that transmit codes rather than card numbers.

- Reduced Churn: Direct bank deductions help mitigate or eliminate payment failures, contributing to improved transaction reliability.

How to make an ACH transfer with FISPAN’s solution

Given that the plugin seamlessly integrates with your ERP system, the interface and menus will already be intuitive and familiar to you.

Beyond managing various payment rails, the plugin takes care of all the specific formatting, security, and handling requirements associated with ACH payments automatically. You can enjoy all these features without any additional effort on your part. Consider it another valuable addition to enhance your range of customer convenience offerings.

Making ACH payments is as easy as:

- Go to the plugin’s Bill Payments window embedded within your ERP.

- Review the pre-populated list of open bills and their default payment methods

(where ACH is a convenient, low-cost option). - Select, filter and group the bills if need be and make any changes.

- Submit the batch for payment.

- Relax and let FISPAN:

-

- Deal with the various file formats, security and payment requirements.

- Run the processes through an internal validation system.

- Communicate directly with your bank to send and receive secure data and status updates so you can track the payment.

- Notify you of any issues or failures, reverse any affected payments and reset them back to the unpaid list.

- Update your general ledger.

- Update the status and history for each vendor and their transaction records to reflect what happened.

- Make this information immediately accessible to the rest of your ERP system including your now much easier reconciliation process.

Other special requirements and rules around approving and releasing payments before funds are transferred are all still applied within your normal bank processes.

Learn more about what FISPAN can do to help streamline your financial processes.